FIVE HOUSING TRENDS WE'RE SEEING SO FAR IN 2011

Depending on whom you speak with, Home Values are still declining.... Home Values have "stabilized".... Home Values are on the rise.... The truth is, it depends!!

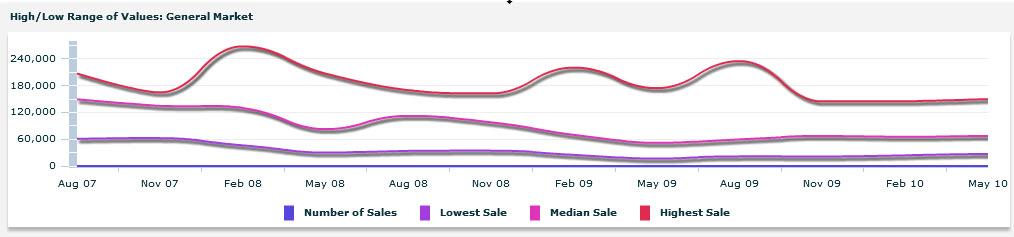

If your looking at housing markets in West Oakland County, or East Livingston County, in general, things are looking up. In most "Micro Markets" (a certain segment based on home size, amenities, etc) we can extract trends that might be considered showing an increase in values. In other Micro Markets, I'm still seeing annual double digit declines. So, the truth is, when it comes to real estate value trends, It Depends. (wait a minute, I already said that)

So what do I see effecting sales and values in the coming year? let's start with..

1. Home owners are holding off on refinancing.

Mortgage refinancing in 2011 is expected to experience a big drop compared with 2010. We're already seeing a marked slowing in refi applications. The prospect of higher interest rates on home loans is one reason for the outlook, but not the only reason. Most Homeowners who have measurable equity, A-1 credit and solid employment have refinanced at least once during 2009 or 2010, locking in low fixed rates and consequently, have little or no incentive to refinance again in 2011.

Those folks who didn't refinance in the last two years due to their loss of equity, unstable employment or damaged credit, probably won't do so this year either because, while still-low rates may create an incentive, those challenges will become even harder to overcome.

2. Home loans are getting harder to get.

There's no secret out there, it's become more difficult to qualify for a home loan today than it was in the past, and it looks like the only changes coming down the road are only going to make it harder.

The tight lending guidelines are the result of lenders' new Conservative attitude toward the risk of bad loans and the real possibility that while they continue to exist, Fannie Mae and Freddie Mac will force the lenders to buy back older, faulty loans, causing them to have less available cash to make new loans.

Lenders are being "Extremely Cautious" and asking for volumes of documentation from borrowers, meaning multiple credit checks, income verifications and appraisals, increasing the cost of acquiring a mortgage from the start.

Borrowers seeking a low down payment loan insured by the Federal Housing Administration (FHA) will also be subject to higher standards in 2011, due in part to lenders addition requirements, commonly called "Overlays".

3. Home buyers will remain on the fence

Now is supposed to be a great time to buy a home. Mortgage rates, for the time being, remain low and prices are the lowest in 10 years. This combination makes real estate relatively more affordable to purchase. Some folks contend that home ownership has never been more affordable.

Plenty of properties are on the market, and inflation, waiting off the horizon to take a big bounce, could boost home values over the long term. Yet many might-be buyers remain on the sidelines due to near-term doubts about the wisdom of buying a home. Indeed, a Fannie Mae survey from the third quarter of 2010 found that one third of those asked said they were more likely to rent rather than buy their next residence. So much for our Government's thought that EVERYONE deserves to own a home.

The recent destabilization in mortgage interest rates, despite the Federal Reserve's efforts keep rates low, should be an alarming event for anyone who wants to buy in the next few years. That alone, should have buyers thinking about buying sooner than later. If rate do jump up, prices may drop even more and make it all a wash, but it's still tough to consider that you may end up taking a mortgage at 7 or 8% while your neighbor is only paying 4%.

4. Home Sellers continue to face "sagging" prices.

Selling a home continues to be a challenge due in part to the loss of qualified buyers and the huge "Shadow Inventory" of homes that are stuck in the foreclosure process, but not yet on the market. As long as these dynamics and high rates of unemployment persist, so will the downward pressure on home prices.

Lower prices may attract more buyers, but many of them won't be able to quality for a home loan. Lower prices could also increase the supply of homes as more owners just walk away from their under water mortgages.

5. Struggling homeowners aren't getting much relief.

Government programs so far have a dismal track record of delivering aid to homeowners who are unable to make their mortgage payment. Our Government has thrown so much of OUR money at this problem, they could have paid off the mortgages of a large percentage of those who applied hoping to get just a little help. Predictions are that this situation won't change much in 2011, due to the intractable nature of the problem.

Homeowners who are under water on their mortgage should contact their loan servicer and ask about a loan modification. Just remember, YOU CAN'T STOP TRYING!

Some borrowers have received relief, but those golden tickets are the exception. More often, the process results in frustration, disappointment and perhaps only a temporary fix at best for the homeowner's situation. There's no guarantee that you'll get a reasonable loan modification, but you might, so it's always worth trying.

Bottom line?

If you can refinance, now is the time.

If you can purchase, now is the time.

If you can sell now is the time.

Have you visited my new web site? http://www.1stinmichigan.com/

Looking for real estate? http://www.hglenbetts.com/